UK Furniture & Flooring Sector Report summary

April 2024

Period covered: Period covered: 25 February – 30 March 2024

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Furniture & Flooring sales

Furniture & Flooring suffered deepening declines at xx% YoY in March according to the Retail Economics Retail Sales Index

Retail Economics forecasts Furniture & Flooring sales to grow xx% YoY in 2024, with sales rising to £xx.

Early Easter

Non-food sales (xx%) edged up in March following xx months of decline. Spending on cosmetics and smaller home items supported sales around Mother’s Day and in preparation for Easter. But non-food sales continues to be dragged by hesitancy to spend on big ticket items.

Furniture & Flooring xxxx of growth rankings, as it faces xxxx. Data showing the wider Households Goods category faced a xx% decline in prices in March.

The category was unable to benefit from a step up in retail footfall in March, fuelled by the earlier Easter weekend. Annual footfall rose by xx% across the UK and xx% at retail parks.

Sentiment to make big ticket purchases slipped two points to xx (GfK), as the Bank of England's base rate remained at a xxxx high of xx% in March. This has seen borrowing costs remain elevated and more households see a jump in housing costs following mortgage and rent renewals, squeezing budgets for home-related spending.

It’s having an acute impact on those transitioning from fixed-rate mortgage deals at average rates of xx% to significantly higher rates typically above xx%, and in part leading to record high rental inflation at xx%.

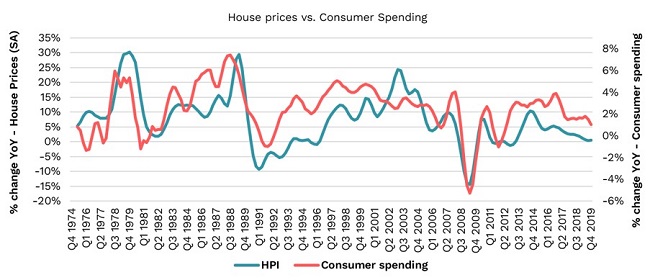

Impact on housing

Currently, over half (xx%) of consumers said they have some concerns with their personal financial situation in April, up xx percentage points from the start of the year (Retail Economics).

Middle- and high-income households are experiencing a moderate recovery in spare cash available for discretionary spending compared to last year – up over £xx per month for the average household (Retail Economics). However, discretionary incomes among average families remain flat on xxxx ago, putting pressure on confidence to make large purchase decisions.

The housing market is subdued, impacting intentions to spend on Furniture & Flooring. Mortgage rates have fluctuated in recent months following a period of softening, as sticky inflation tempers optimism around the timing of interest rate cuts by the Bank of England.

Take out a FREE 30 day membership trial to read the full report.

Strong relationship between house prices and consumer willingness to spend

Source: ONS

Source: ONS